Statistics tasks

An analytician is studying the profits of a company over the course of ten years. Let X be the number of years after the inital year the analytician is studying. Y is the profits in year X and the analytician believes the profits are a normal distribution stochastic(random) variable with expectation 𝐸(𝑌)=𝛽0+𝛽1𝑥 and standard deviation 𝜎=0.08. Based on these observations the analytician finds that:

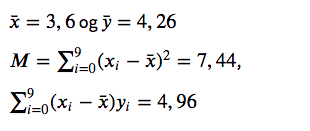

𝑥¯=3.6 and 𝑦¯=4.26

𝑀=∑^9_𝑖=0 (𝑥𝑖−𝑥¯)^2=7.44,

∑^9_𝑖=0 (𝑥𝑖−𝑥¯)𝑦𝑖=4.96

(I added this as a picture too as I have a hard time writing formulas on here)

Questions:

1. Estimate 𝛽0 og 𝛽1.

2. Can it be proven that the yearly increase in profits, 𝛽1, is bigger than 0.5? Formulate fitting hypothesis and do a hypothesis test at 0,5% significance level.

Critical value=

H1 or not H1?

3.Find a 99% confidence interval for expected profits for x=5

Upper confidence limit:

Lower confidence limit:

4. Find a 95% prediction interval for expected profits for x=1

Upper prediction limit:

Lower prediction limit:

𝑥¯=3.6 and 𝑦¯=4.26

𝑀=∑^9_𝑖=0 (𝑥𝑖−𝑥¯)^2=7.44,

∑^9_𝑖=0 (𝑥𝑖−𝑥¯)𝑦𝑖=4.96

(I added this as a picture too as I have a hard time writing formulas on here)

Questions:

1. Estimate 𝛽0 og 𝛽1.

2. Can it be proven that the yearly increase in profits, 𝛽1, is bigger than 0.5? Formulate fitting hypothesis and do a hypothesis test at 0,5% significance level.

Critical value=

H1 or not H1?

3.Find a 99% confidence interval for expected profits for x=5

Upper confidence limit:

Lower confidence limit:

4. Find a 95% prediction interval for expected profits for x=1

Upper prediction limit:

Lower prediction limit:

Answer

Answers can only be viewed under the following conditions:

- The questioner was satisfied with and accepted the answer, or

- The answer was evaluated as being 100% correct by the judge.

The answer is accepted.

Join Matchmaticians Affiliate Marketing

Program to earn up to a 50% commission on every question that your affiliated users ask or answer.

- answered

- 1726 views

- $5.41

Related Questions

- A miner trapped in a mine

- Intro to stats symmetry vs skew and missing data values questions

- How do we describe an intuitive arithmetic mean that gives the following? (I can't type more than 200 letters)

- 2 conceptual college statistics questions - no equations

- Explain how the binomial probability equation is $\frac{n!}{x!(n-x)!}(p^x)(q^x)$

- How to use bootstrap techniques to criticise a linear model?

- Introductory statistics, probability (standard distribution, binomial distribution)

- Find a number for 𝛼 so f(x) is a valid probability density function