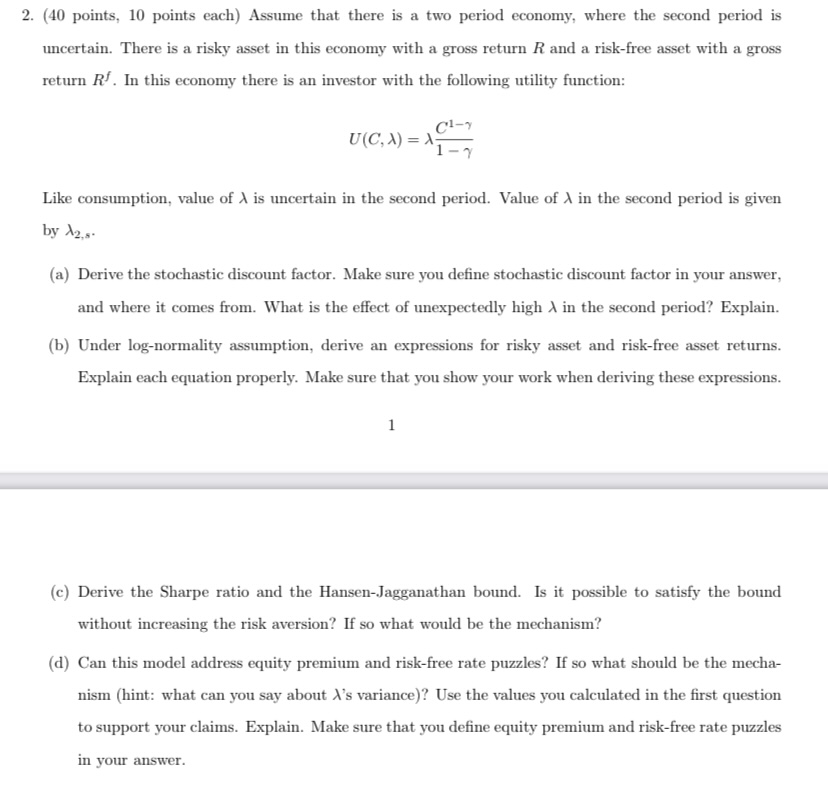

Consumption based asset pricing model stochastic discount factor derivation

This is an undergrad finance level question. Lecture notes :

https://drive.google.com/file/d/1GdZwD0QKRMKdSa2HoT0qn5HWO7WbVWIj/view

Join Matchmaticians Affiliate Marketing

Program to earn up to a 50% commission on every question that your affiliated users ask or answer.

- closed

- 1397 views

- $19.38

Related Questions

- Compound Interest with monthly added capital

- Amortization Table

-

Mathematical finance question on Portfolio

and Investment Year Methods(question attached below) -

You are given:

(i) X is the current value at time 2 of a 20-year annuity-due of $1 per annum.

(ii) The annual effective interest rate for year t is (1/(8+t)).

Find X. - Disecting Constant Product formula

- Solving Constant Product for ratio

- Contract Crediting Rate Formula

- Make a graphical of analysis of the Strong Axiom of Revelead Preference

The bounty is low for a high level question with multiple parts.

At least could you do the first 2-3 parts?

Please provide the lecture notes.

I shared the lecture notes