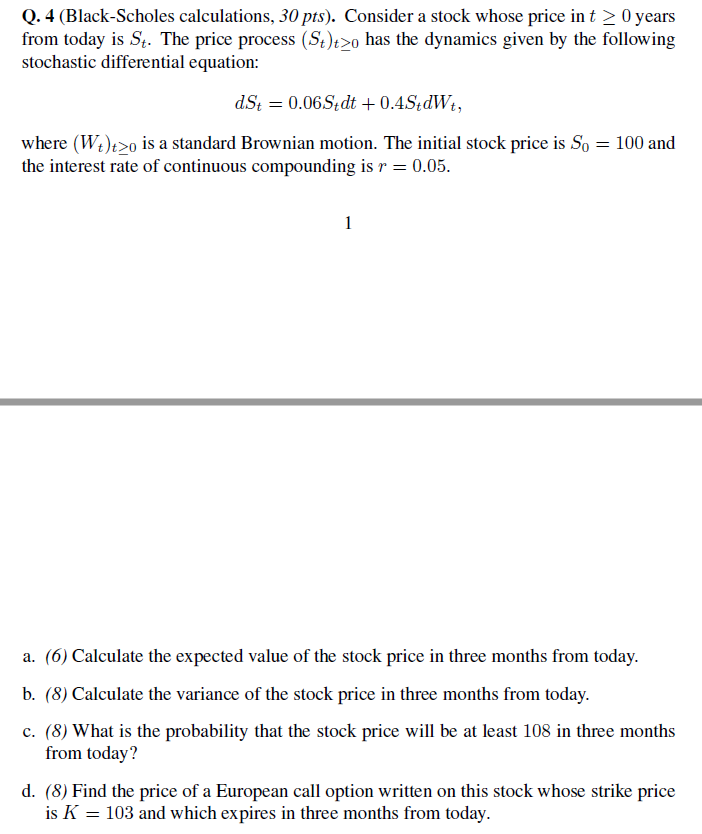

Black Scholes Calculation

This is a question from my introduction to finance class. I need to use Ito calculus but I don't know how to use it.

Answer

Answers can only be viewed under the following conditions:

- The questioner was satisfied with and accepted the answer, or

- The answer was evaluated as being 100% correct by the judge.

1 Attachment

3.7K

-

Should not it be that solution to SDE is : St=S0*e^(mü*t+sigma*Wt) instead of your solution. I mean I guess your solution is seems to bo correct but this is what my lecture notes tells me. Or I am not sure even both things mean the same thing or not, could you clarify this?

-

The solution is not quite like you say. A straight forward reference is Wikipedia: https://en.wikipedia.org/wiki/Geometric_Brownian_motion Also, the book Stochastic Differential Equations by Oksendal, page 62.

The answer is accepted.

Join Matchmaticians Affiliate Marketing

Program to earn up to a 50% commission on every question that your affiliated users ask or answer.

- answered

- 1479 views

- $14.76